Distributive Analysis of Budget 2025’s Cost-of-Living and Tax-Benefit Measures

Budget 2025, announced in October 2024, was the final budget of the outgoing coalition Government and was presented as some aspects of the cost-of-living crisis continued to challenge households across Irish society. Like Budgets 2023 and 2024, it contained a mixture of measures that took effect before the end of that year and measures that took effect from the start of 2025. In this analysis we bring together this range of announced policies to consider their cumulative effect on the income of households.

Distributive Analysis of Budget 2025’s Cost-of-Living and Tax-Benefit Measures

The measures we examine capture:

- The household energy credit paid to all households in late 2024, once off increases in welfare payments (two double child benefit payments, lump sum payments to recipients of the fuel allowance, living alone allowance and qualified child increase) made before the end of 2024, and the Christmas bonus welfare payment. These are collectively referred to as ‘Budget 2025 for 2024’ measures.

- The household energy credit paid to all households in early 2025, plus changes taking effect from January 1st to welfare rates and income taxation (via changes to bands, credits, the USC and PRSI). These are collectively referred to as ‘Budget 2025 for 2025’ measures.

The households we examine are those tracked annually in our income distribution model. They are spread across all areas of society and capture those with a job, families with children, those unemployed and pensioner households. Within those households that have income from a job we include workers on incomes ranging from €30,000 to €200,000; €30,000 is almost equivalent to the living wage for a single worker. In the case of working households, the analysis is focused on PAYE earners only.

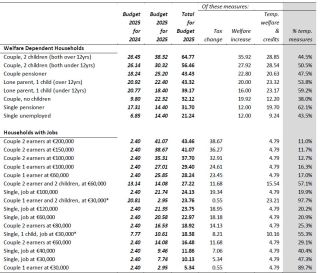

Table 1: Combined Weekly Impact (€) of Budget 2025 Cost-of-Living Measures and Tax-Benefit Changes

Source: Social Justice Ireland Income Distribution Model. Notes: Table includes all measures announced as part of Budget 2025 including measures for the remainder of 2024 (Budget 2025 for 2024) and those for all of 2025 (Budget 2025 for 2025). Each household category is sorted by the size of the overall Budget 2025 package. Temporary measures include once-off welfare payments and household energy credits. Tax changes includes changes to income taxes and PRSI. *Depending on circumstances, these household may also be entitled to the Working Family Payment.

Overall, the total weekly impact on the households examined is large, ranging from €21 to €65 a week for welfare dependent households and from €5 to €43 a week for households with jobs. Within welfare dependent households the largest disposable income gains have been received by those with children. Among working households tax changes have favoured those with income subject to the higher income tax rate.

As part of our budgetary policy engagement over recent years, Social Justice Ireland has highlighted that there is a marked difference in the way that recent budgetary choices have delivered income changes to households. They have included temporary measures, such as electricity credits and one-off additional welfare related payments, alongside permanent measures such as changes to the value of core welfare payments and changes to tax credits, tax bands and PRSI rates. The new Government (appointed in early 2025) has made it clear that these temporary measures will be discontinued as the cost-of-living crisis fades, however, the income effect of the permanent changes will remain. Consequently, we think it is important to consider the distributive impact of the Budget taking account of these differences; something that Government has failed to do through the recent set of cost-of-living crisis Budgets.

Table 1 decomposes the Budget 2025 household income changes to examine whether they are associated with permanent changes to income taxation and welfare rates, or temporary measures. It shows that temporary measures are more concentrated among welfare dependent households and those at work but on low incomes. Conversely, the income gains received by higher income working households are much more associated with permanent measures (income taxation reductions). For example, temporary measures represented between 47-62% of the income gains for pensioners but only 11-16% of that received by couples with incomes over €100,000. Once the temporary measures disappear, the income effect associate with these permanent measures will remain and notably widen Irish societies income divisions.

A notable finding is that Budget 2025 provided least for the large cohort of lower income workers; those earning above the minimum wage but below annual income levels that allow them to experience much of the value of the income tax changes. A group earning around €15 to €20 per hour (€30,000 to €40,000 per annum). Year after year this large group of workers hears of ‘gains’ from the Budget but experiences little if any of them; something that cannot persist both due to its distributive effects and the socio-political reality that we cannot keep ignoring these workers and families. Social Justice Ireland has continually highlighted the relevance of refundable tax credits as a means of making the taxation system fairer and helping this low-income group.

Overall, Budget 2025 followed Budgets 2023 and 2024 in taking this approach to the distribution of resources. It is one that Social Justice Ireland regrets. Although the Budgets have been progressive and successful in the short-term, by providing much needed help to households struggling to make ends meet, their longer-term legacy will be to widen further the gap between the better off and those on the lowest welfare and work incomes.