Who has benefitted from Budget income tax changes?

With much focus at present on income tax, and the potential for changes in the forthcoming budget it is worthwhile in looking at the distribution of budgetary income tax changes to date. Budget 2023 contained a number of notable reductions to income taxes with a large increase in the standard rate tax band alongside smaller changes which increased tax credits and decreased the USC. These are the latest in a series of changes to income tax in Budgets since 2014. So who has gained from the changes in Budget 2023, and from all the other income tax decreases provided over most Budgets since 2014?

Income tax changes 2014-2023

Budget 2023 contained a number of notable reductions to income taxes with a large increase in the standard rate tax band alongside smaller changes which increased tax credits and decreased the USC. Following that Budget Social Justice Ireland has examined who gained from it and all the other income tax decreases provided over most Budgets since 2014. We provide the results of that analysis here. Over three diagrams we compare the total annual value of these reductions between 2014 and 2023.

The analysis captures changes to income tax rates, USC rates, social insurance rates and structures, and income tax credits. For example, a single earner with a gross income of €40,000 paid €9,920 in income taxes, employee PRSI and USC in 2014 and paid €7,080 in 2023; a reduction of €2,840.

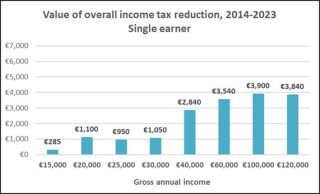

Single earner:

- Over the period 2014-2023 a single earner on €120,000 has seen an income tax reduction to the value of €3,840;

- Over the period 2014-2023 a single earner on €60,000 has seen an income tax reduction to the value of €3,540;

- Over the period 2014-2023 a single earner on €30,00 has seen an income tax reduction to the value of €1,050;

- Over the period 2014-2023 a single earner on €25,00 has seen an income tax reduction to the value of €950.

Chart 1

Source: Department of Finance Budget Documents - various years.

Notes: PAYE workers. For couples with 2 earners the income is assumed to be split 65%/35%.

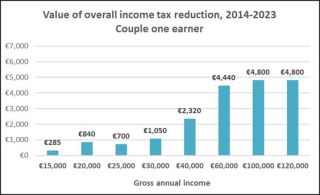

Couple with one earner:

- Over the period 2014-2023 a couple with one earner on €120,000 have seen an income tax reduction to the value of €4,800.

- Over the period 2014-2023 a couple with one earner on €60,000 have seen an income tax reduction to the value of €4,440.

- Over the period 2014-2023 a couple with one earner on €40,000 have seen an income tax reduction to the value of €2,320.

- Over the period 2014-2023 a couple with one earner on €30,000 have seen an income tax reduction to the value of €1,050.

Chart 2

Source: Department of Finance Budget Documents - various years.

Notes: PAYE workers. For couples with 2 earners the income is assumed to be split 65%/35%.

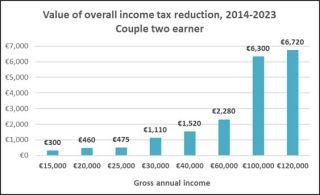

- Couple with two earners:

- Over the period 2014-2023 a couple with two earners on €120,000 have seen an income tax reduction to the value of €6,720.

- Over the period 2014-2023 a couple with two earners on €100,000 have seen an income tax reduction to the value of €6,300.

- Over the period 2014-2023 a couple with two earners on €60,000 have seen an income tax reduction to the value of €2,280.

- Over the period 2014-2023 a couple with two earners on €40,000 have seen an income tax reduction to the value of €1,520.

- Over the period 2014-2023 a couple with two earners on €30,000 have seen an income tax reduction to the value of €1,110.

Chart 3

Source: Department of Finance Budget Documents - various years.

Notes: PAYE workers. For couples with 2 earners the income is assumed to be split 65%/35%.

The analysis highlights a number of points.

First, it provides evidence of the scale of the income tax reductions delivered over recent years; these are often overlooked, yet are substantial at the individual/household level and at the exchequer level.

Second, the charts illustrate the distribution of these income tax decreases. As we have highlighted in our annual budget documents the gains have been skewed to higher income earners and households. Any discussions on income tax changes in future budgets should take account of those changes that have already been made and where the benefits of those changes have gone.