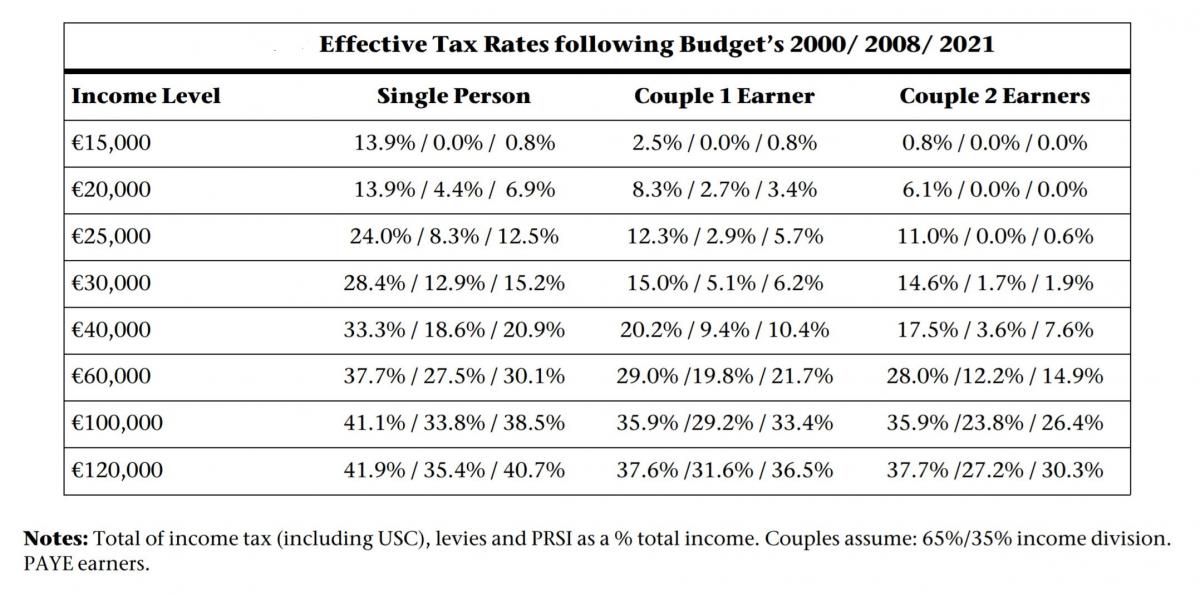

Effective income tax rates after Budget 2021

Central to a thorough understanding of income taxation in Ireland are effective tax rates.

These rates are calculated by comparing the total amount of income tax a person pays with their pre-tax income. For example, a person earning €50,000 who pays €10,000 in taxation (after all their credits and allowances) will have an effective tax rate of 20 per cent. Calculating the scale of income taxation in this way provides a more accurate reflection of the scale of income taxation faced by earners.

Following Budget 2021 we have calculated effective tax rates for a single person, a single income couple and a couple with two earners. The table below presents the results of this analysis. For comparative purposes, it also presents the effective tax rates which existed for people with the same income levels in 2000 and 2008.

In 2021, for a single person with an income of €15,000 the effective income tax rate will be 0.8%, rising to 12.5% of an income of €25,000 and 40.7% of an income of €120,000. A single income couple will have an effective income tax rate of 0.8% at an income of €15,000, rising to 5.7% at an income of €25,000, 21.7% at an income of €60,000 and 36.5% at an income of €120,000. In the case of a couple where both are earning and their combined income is €40,000 their effective income tax rate is 7.6%, rising to 30.3% for combined earnings of €120,000.

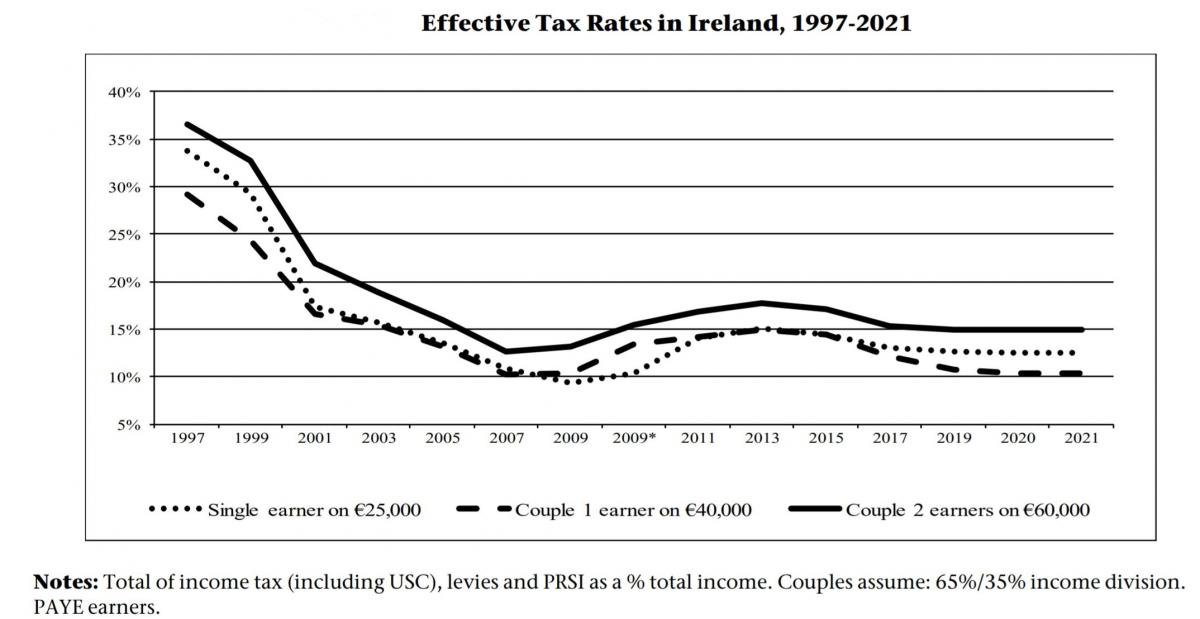

As the chart below shows, despite increases during the last economic crisis, effective income tax rates have decreased considerably over the past two decades for all earners.