Fairer Income Tax Choices were Possible in Budget 2019

Budget 2019 included an income tax package with a full year cost of €356m (€123m on USC reductions, €161m on income tax reductions and €72m on credit increases).

Social Justice Ireland's analysis of Budget 2019 (see pages 4, 6 and 7) shows that these changes are skewed and provide larger gains to those on higher incomes compared to those on lower incomes. For example, a single person earning €25,000 gains €26.62 per annum while a single person on €75,000 gains almost 11 times more (€289.23 per annum).

For the same commitment of resources that the Government allocated to reforming these income taxes (€356m) Government could have chosen a much fairer set of alternatives. These include:

- Refunding the unused proportion of PAYE and personal tax credits to those who are active in the labour market but earn insufficient income to use up all these tax credits (i.e. introduce a system of refundable tax credits): full year cost of €140m

- Increase the personal tax credit for all earners by €85 per annum: full year cost of €216m

Our costings for these measures are based on a previous Social Justice Ireland study on refundable tax credits (see p5 of our pre-Budget Budget Choices document) and the recently released Revenue Commissioners Ready Reckoner for Budget 2019.

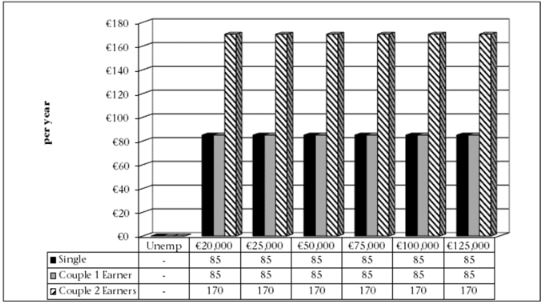

The costing of the €85 per annum increase in the personal tax credit also assumes a commensurate increase in the married persons, widowed persons and lone parent credit. The full year cost of this increase according to the Revenue Commissioners is €216m. The distributive impact of this alternative policy choice is outlined in the chart below.

.

.

It provides an increase of €85 per annum to all single earners and couples with one earner. Couples with two earners gain twice this amount, €170 per annum. In contrast to the Budget outcomes (see p6-7):

- a single person earning €25,000 gains €85 per annum;

- a single person earning €75,000 also gains €85 per annum.

Below €16,500, single earners experience further gains due to a refund of unused tax credits. As the chart shows, a fairer tax package could have delivered the same amount of income gains to all single earners above €16,500. Proportionally, such a gain is greater for lower income earners reflecting a more progressive distribution of budget income tax resources.

As our analysis shows, for the same allocation of resources, the Government could have chosen a fairer and more equitable income tax package in this Budget. We regret that Government ignored this option. The skewed outcome of the income tax measures in Budget 2019 could have been avoided. A fairer alternative was available.