Latest Central Bank data shows mortgages held by non-bank entities has more than doubled since 2016

At the end of 2018, there were 63,426 home mortgages in arrears (not including buy to lets), with 44,009 of these in arrears of more than 90 days. This represents a 11.5% decrease on the previous year, for both all mortgage accounts in arrears and those in arrears of more than 90 days.

111,504 home mortgages are in restructured arrangements (a decrease of 6% on Q4 of 2017), with 33% having had their arrears capitalised (that is, where the arrears are added to the outstanding balance of the mortgage and repayments recalculated based on this higher amount), 23.7% on reduced payments, 17.3% classified as ‘Other’ (which can include reduced repayment arrangements or temporary arrangements) and 24.3% on ‘split mortgages’. Households with ‘split mortgages’ are most precarious where it is unlikely that they will experience a change in financial circumstances over the term of the loan and will therefore be dependent on realising the equity at the end of the warehoused period in order to pay the amount due. These families will then be faced with the prospect of selling their family home when they are at or close to retirement age.

By the end of 2018, 1,500 residential properties were in possession of institutions. Of the 161 family homes repossessed during this quarter, 42% were on foot of a court order, with the remaining 58 per cent being voluntarily surrendered or abandoned.

Mortgage Arrears – Non-bank Entities

However, when we look behind the figures it is clear that some mortgages are more precarious than others. Non-bank entities held 84,658 family home mortgages, of which 25,469 are held by unregulated loan owners. This represents an increase of 73% on all family home mortgages held by non-bank entities at the end of 2017. Of the 84,658 family home mortgages, 20% are in arrears, with 15.5% in arrears of more than 90 days.

The mortgages held by unregulated loan owners are more likely to be in severe arrears situations. 29% of home mortgages held by unregulated loan owners are in arrears of more than 90 days, with 23% in arrears more than 720 days. This compares with 9.7% and 5.4% respectively for those home mortgages held by retail credit firms and 4.7% and 2.8% respectively for banks. Due to the nature of such funds, whose motives are profit-driven, repossessions are likely to be more prevalent among this cohort, resulting in greater need for social housing.

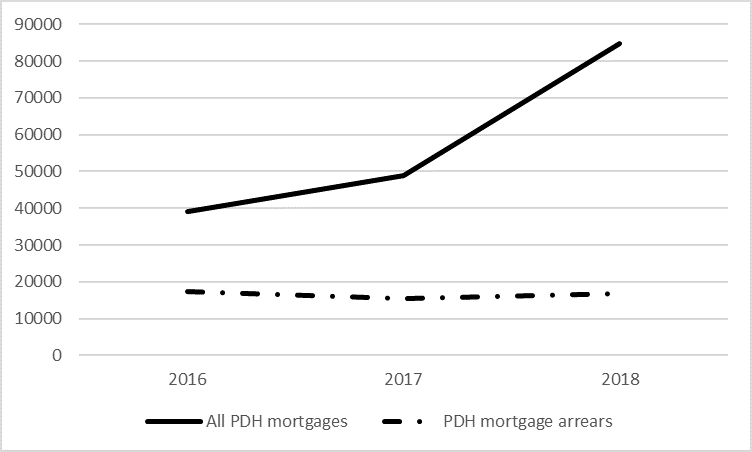

There has been much commentary recently about the sale of mortgage loans by banks to non-bank entities as part of a strategy to reduce the number of non-performing loans (NPLs) to within EU parameters. Consumer advocates have expressed concerned about the lack of consumer protections for borrowers, particularly those whose loans were performing, while those in favour of this strategy cite the high level of NPLs acting as a barrier to accessing better credit terms, thereby contributing to Ireland’s high mortgage rates. Data extracted from the Central Bank’s quarterly statistical report on mortgage arrears show that while the number of PDH mortgages held by non-bank entities has more than doubled since 2016 (an increase of 116%), the number in arrears has actually decreased slightly (Chart 1).

Chart 1: PDH Mortgages held and Mortgage Arrears, Non-Bank Entities, 2016 to 2018

Source: Central Bank of Ireland, Residential Mortgage Arrears and Repossession Statistics.

While some efforts were made to include non-bank entities within the remit of consumer protection legislation and regulation, the reality is that for the increasing number of borrowers whose loans are held by unregulated loan owners, these simply do not apply.