Mortgage Arrears - 35,000 people at risk of homelessness

Research released today by the Central Bank of Ireland shows that 44 percent of mortgages in late stage mortgage arrears, over 12,700 households (c.34,969 people), are now more than five years in arrears.

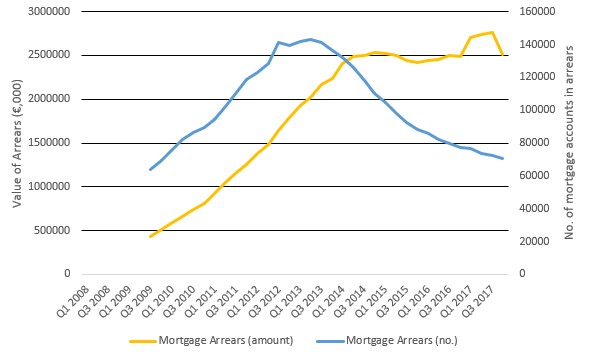

If long term sustainable solutions to mortgage arrears are not found, many more families will find themselves in need of social housing. There were 70,488 home mortgages in arrears at the end of 2017 with Central Bank regulated lenders, with 48,433 in arrears of more than 90 days. While the number of mortgages in arrears has been decreasing for the past 17 consecutive quarters, the actual amount of arrears continued to rise, reaching a high of €2.76 billion in Q3 2017, before decreasing to €2.5 billion by the end of the year.

In the same period, 118,477 home mortgages were in restructured arrangements, with over half on reduced payments of which 23.2 per cent were ‘split mortgages’. Households with ‘split mortgages’ are most precarious where it is unlikely that they will experience a change in financial circumstances over the term of the loan and will therefore be dependent on realising the equity at the end of the warehoused period in order to pay the amount due. These families will then be faced with the prospect of selling their family home when they are at or close to retirement age.

By the end of 2017, 1,717 homes were in the possession of Central Bank lenders, with 311 of these having been taken into possession in the last quarter of the year.

Non-bank entities held 61,446 mortgages over homes and investment properties, of which 47,820 are homes. 25 per cent of all mortgages are now held by non-bank entities, with 9 per cent held by ‘retail credit firms’ and 16 per cent with ‘unregulated loan owners’. Due to this unregulated status, the borrowers concerned, many of whom are in dire arrears situations (42 per cent of home mortgages held by unregulated loan owners are 720 days in arrears, six times the rate of home mortgages held by regulated retail credit firms with that level of arrears), have been stripped of even the most basic consumer protections. Due to the nature of such funds, whose motives are profit-driven, repossessions are likely to be more prevalent among this cohort, resulting in greater need for social housing.

There are already almost 10,000 people accessing emergency accommodation, at an accommodation cost of over €112 million in 2017 alone, according to available data.

Government reliance on temporary measures and private rented accommodation is not working. Increased supply of affordable, sustainable accommodation is the only solution.