Need for personal debt taskforce as thousands lose their jobs in the wake of COVID-19

Defining the Problem

There is no official definition of over-indebtedness in Ireland. In his 2009 study, Stamp provided an expansive definition with reference to a 2008 study undertaken by a consortium of European organisations in the personal finance area, namely[1]:

People are over-indebted if their net resources (income and realisable assets) render them persistently unable to meet essential living expenses and debt repayments as they fall due.

The study then outlines five key measurements of over-indebtedness contained in the 2008 study, as:

- Persistency (a prolonged as opposed to once-off problem)

- Lack of payment capacity (an inability to meet debt-related payments and other commitments)

- Problems with a range of contractual financial commitments (defined broadly to include mortgages, household bills and consumer credit)

- An inability to maintain a reasonable standard of living (i.e. an inability to live reasonably and maintain debts)

- Illiquidity (an inability to realise assets to discharge outstanding debts)

The expansion of available credit with lax regulation was a key driver in the financial crisis of 2008. When that crisis hit, and with it a sharp rise in unemployment, thousands of households experienced difficulties paying bills and everyday expenses. Lessons were learnt that resulted in the constriction of mainstream credit, however half a million people were living in households in arrears on at least one bill in 2018 as we face another wave of job losses due to the COVID-19 outbreak.

Measuring the Problem

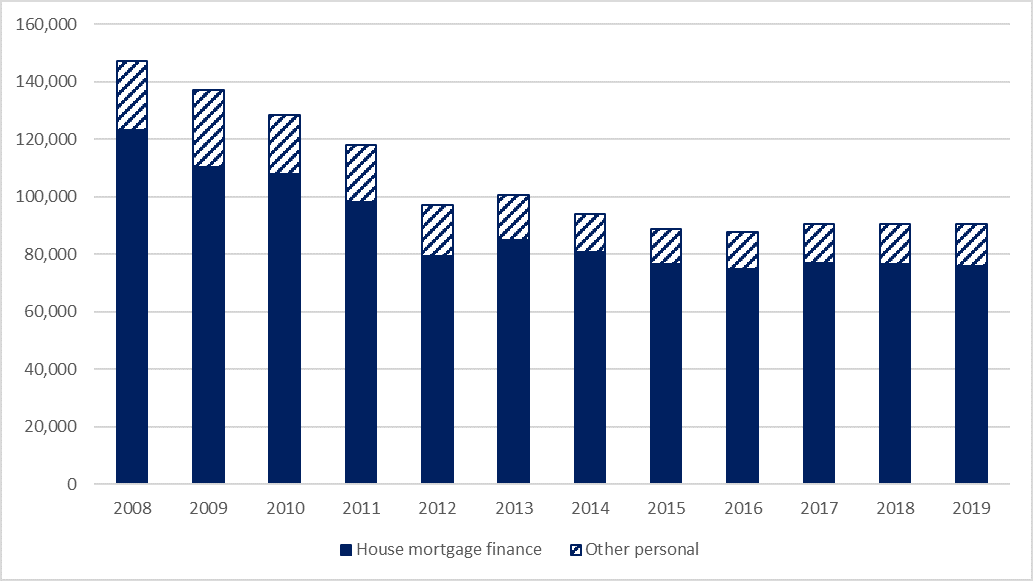

At the time of the 2008 crash, Central Bank-regulated lending to private households exceeded €147 billion, the majority of this being mortgage finance (€123 billion) and the remainder for “other personal” finance (€24 billion). In the years since, the constriction of mainstream personal credit resulted in the paying down of outstanding balances, rather than further borrowing, and a levelling-off of the total outstanding to the region of €90-100 billion. As of September 2019, the total amount of Central Bank-regulated credit to Irish private households was €90.4 billion (Chart 1).

Chart 1: Credit to Irish Private Households, Outstanding Amounts (€ million), 2008 to 2019

Source: Analysis of Central Bank Private Household Credit and Deposit data, various years.

Notes: Data for September each year.

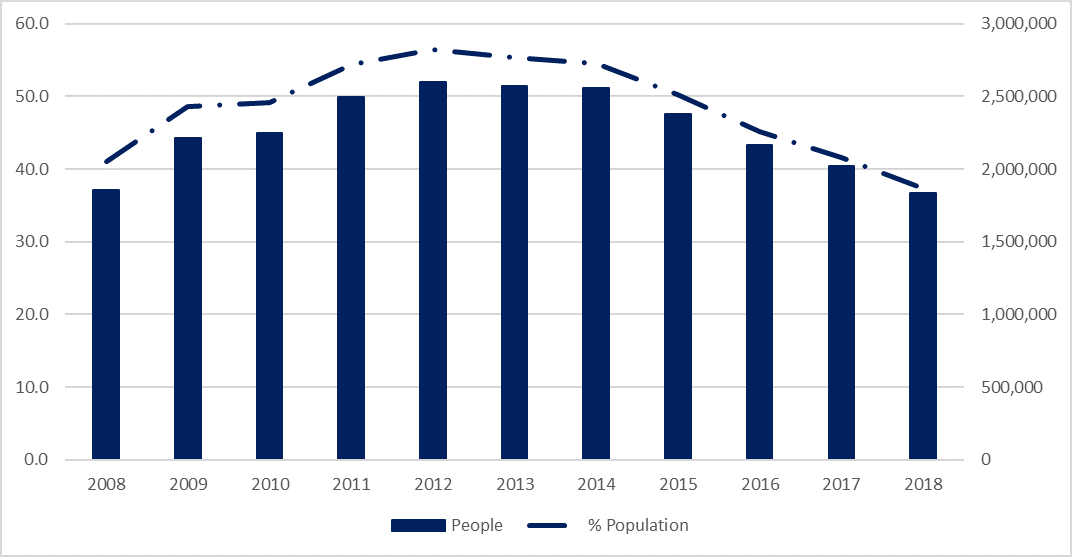

While this would appear to show that the Irish population is in a better position now to deal with financial shocks than it was just over a decade ago, with less credit with which to get into difficulty, the reality is that almost the same number of people were living in households which reported being unable to face an unexpected financial expense in 2018 (at a time of almost full employment) as in 2008 (1.83 million in 2018 compared to 1.85 million in 2008).

This proportion rose steadily between 2008 and 2012, where it reached 56.4 per cent, before declining to 37.3 per cent in 2018 (Chart 2).

Chart 2: Inability to face unexpected financial expenses, % Population and No. of People, 2008 to 2018

Source: Analysis of Eurostat [ilc_mdes04], Central Statistics Office Population Estimates (Persons in April) by Age Group, Sex and Year [PEA01]

Notes: Calculation of people based on population data for April of the following year

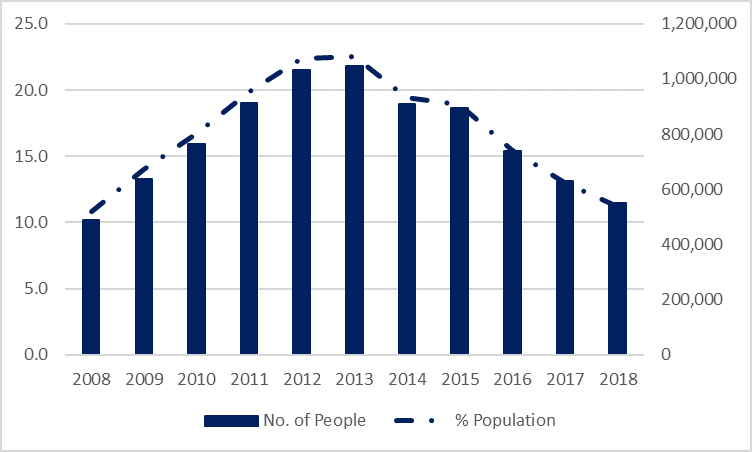

These financial difficulties are further compounded for those who are already in arrears on one or more of their bills. In 2018, 11.2 per cent of the population, some 551,208 people, were in households with arrears on mortgage or rent, utility bills or loan payments, compared to 489,607 people (10.8 per cent) in 2008 (Chart 3). That is over 61,000 more people.

Chart 3: Arrears on mortgage or rent, utility bills or loan payments, % Population and No. of People, 2008 to 2018

Source: Analysis of Eurostat [ilc_mdes05], Central Statistics Office Population Estimates (Persons in April) by Age Group, Sex and Year [PEA01]

Notes: Calculation of people based on population data for April of the following year

A breakdown by type of debt shows that, despite a return to full employment and a constriction of mainstream credit, the personal debt situation of Ireland’s households is very similar to what it was in 2008 (Table 1).

Table 1: Arrears by Type of Debt, % Population and No. of People, 2008 and 2018

Source: Analysis of Eurostat [ilc_mdes06, ilc_mdes07, ilc_mdes08], Central Statistics Office Population Estimates (Persons in April) by Age Group, Sex and Year [PEA01]

Notes: Calculation of people based on population data for April of the following year

The data available from the Central Bank and the EU-SILC survey relates to “formal” sources of credit. For many low-income households, restrictions on borrowing from mainstream lenders and an inability to provide for contingency savings means finding alternative sources of credit. A report from the Social Finance Foundation found that in 2018 there were 330,000 people accessing credit from moneylending firms[2]. The majority were female, aged between 35 and 54 and drawn from lower socio-economic backgrounds. A large proportion have loans from ‘home credit companies’ which charge APRs of up to 287%. These alternative sources of credit are often prioritised, irrespective of interest rate or associated risks, as providing easier access to emergency funds and a personal connection with the creditor[3].

Policy responses to problem personal debt have been patchy at best. A review of MABS Clients in Mortgage Arrears published in 2013[4] highlighted the difficulties experienced by MABS clients in mortgage arrears in coming to a new payment arrangement with their lender. These difficulties were caused from a range of issues, indicating a lack of training on the part of front-line bank staff, a lack of understanding of financial terms among borrowers, and delays by lenders in processing requests for support. A lack of understanding of financial terms was also raised in a report into non-mortgage debt published by TASC earlier this year[5], with the need to support greater financial capability among consumers were themes explored in both a report published by the Competition and Consumer Protection Commission[6] and the recent Civil Society Roundtable hosted by the Central Bank[7].

In the wake of the coronavirus, the Central Bank of Ireland urged banks to give payment breaks to borrowers whose jobs may have been affected. Ensuring that these breaks are processed quickly and that the terms and conditions attached are easily understood must be a priority.

In addition, the MABS report highlighted other issues experienced by households in debt, including relationship breakdown, mental and physical health issues and addictions. It is therefore concerning that the recommendations of the 2011 Mental Health Commission report on the mental health impacts of problem debt[8] are yet to be fully implemented.

Addressing the Problem

Supporting over-indebted households requires a holistic, whole-person approach. A National Taskforce on Over-indebtedness is required, focusing on prevention of chronic over-indebtedness to the extent that it impacts the health and well-being of individuals and the potential re-growth of the economy after the crisis has passed. This will involve participation from all stakeholders to deal not only with the gaps identified in existing policies, but to develop policies for areas that have not yet been addressed (for example, illegal moneylending).

This Taskforce could have dedicated workstreams such as:

- Mortgage Debt and Mortgage Arrears, to review and strengthen existing policies in this area and to ensure that mortgage borrowers granted a temporary payment break due to COVID-19 are not penalised with interest payments into the future;

- Non-mortgage debt, to include a review and policy response to problems with both formal and informal non-mortgage debt;

- Personal Insolvency to consider the efficacy of the Personal Insolvency Act, 2012 (as amended), particularly for lower-income households;

- Mental and Wellbeing to review the implementation of the findings from their 2011 report in the wake of increased anxiety due to the pandemic and its resultant financial impacts; and

- Financial Inclusion to consider the availability of social lending; the extension of the Basic Payment Account, the introduction of a Minimum Income Standard and the development of money management education programmes.

The work of the Taskforce would be overseen by a Steering Group, consisting of participants from all sectors, who would work to defined Key Performance Indicators to ensure that robust policies and procedures were implemented within specified timeframes.

Addressing the area of over-indebtedness should be a Government priority, effecting as it does not only the health and wellbeing of the individual, but the efficacy of economic recovery.

[1] Stamp, S (2009): A policy framework for addressing over-indebtedness. Combat Poverty Agency: Dublin

[3] Collard, S. and Kempson, E. (2005): Affordable credit for low-income households, University of Bristol

[4] Bennett, C. (2013): MABS Clients and Mortgage Arrears: A profile of MABS clients in mortgage difficulty and factors associated therewith. MABS National Development Limited: Dublin

[5] Lajoie, A. (2020): Exploring Household Debt in Ireland: The Burden of Non-Mortgage Debt & Opportunities to Support Low-Income Households. TASC: Dublin

[6] Competition and Consumer Protection Commission (2018): Financial Capability and Well-being in Ireland in 2018

[7] https://www.centralbank.ie/events/event-detail/2019/11/29/default-calend...

[8] Mental Health Commission, 2011: The Human Cost, An overview of the evidence on economic adversity and mental health and recommendations for action. Mental Health Commission: Dublin