No Consent, No Sale – Any Hope?

The Oireachtas is currently considering the ‘No Consent, No Sale Bill’ which, according to its own preamble is ‘An Act to provide that Lenders may not transfer mortgages on residential property without the consent of the borrower and to provide for related matters.’. This Bill provides that a mortgage on residential property (which would apply to both private dwelling house mortgages and mortgages over buy to let residential property) shall not be transferred without the consent of the borrower. The Bill further provides that, when asking for this consent, the lender must provide enough information to the borrower to allow them to make an “informed decision”, including

(i) a clear explanation of the implications of a transfer including with respect to the borrower’s membership status where the lender is a building society; and

(ii) how the transfer might affect the borrower.

While the Central Bank is envisaged as having a role in approving this explanation, it must be tailored to the individual circumstances of the borrower, who will then be given reasonable time to make a decision.

There are further provisions in respect of lenders acting as servicing agent for the new mortgage owner and additional consent requirements where the lender loses control over the setting of interest rates and arrears handling.

The Bill also sets out in some detail in section 6 what information should be provided by the lender to the borrower and, in section 7, the proposed terms of any transfer agreement.

However, the Governor of the Central Bank, Mr. Philip Lane; the Department of Finance; and other commentators have expressed concern about the impact the Bill will have on the mortgage market here in Ireland, given that our mortgage interest rates are among the highest in the EU. There have also been suggestions that the consumer protections sought in the Bill already exist. This is simply not the case.

Consumer Protection (Regulation of Credit Servicing Firms) Acts, 2015 and 2018

In 2015, in response to the increasing presence of funds in the Irish mortgage scene, the Government introduced the Consumer Protection (Regulation of Credit Servicing Firms) Act. This Act applies to credit servicing firms acting in an administrative capacity on behalf of loan owners and, since 2018, the loan owners themselves (who must be authorised as a credit servicing firm) to ensure that current consumer protections will follow the loan, and the borrower will not be at a disadvantage. These extend to the Consumer Protection Code, 2012; the Code of Conduct on Mortgage Arrears, 2013; the Central Bank (Supervision and Enforcement) Act, 2013; and the Minimum Competency Code 2017. In terms of mortgage transfers, the two codes of most relevance are the Consumer Protection Code, 2012 (particularly where the mortgage is not in arrears) and the Code of Conduct on Mortgage Arrears, 2013.

Consumer Protection Code, 2012 - Statutory Code

The 2012 Consumer Protection Code replaces the previous 2006 version. Since its introduction, there have been six Addendums made to it to provide for the implementation of national law (such as the 2015 Act referenced above) and EU regulation. For the purpose of mortgage transfers, provision 3.11 states (emphasis added):

Where a regulated entity intends to cease operating, merge with another, or to transfer all or part of its regulated activities to another regulated entity it must:

a) notify the Central Bank immediately;

b) provide at least two months notice to affected consumers to enable them to make alternative arrangements;

c) ensure all outstanding business is properly completed prior to the transfer, merger or cessation of operations or, alternatively in the case of a transfer or merger, inform the consumer of how continuity of service will be provided following the transfer or merger; and

d) in the case of a merger or transfer of regulated activities, inform the consumer that their details are being transferred to the other regulated entity, if that is the case.

Essentially, the lender has to provide the borrower with two months’ notice that the mortgage is being transferred. There is no provision for additional information as to the name and address of the loan owner; the relationship between the current and new loan owner; a description of the business activities, including how long they have been operating, of the new loan owner; details of policies and procedures that will apply for the setting of interest rates and making repayments; and a statement that in the absence of any consent, the existing arrangement will apply.

Code of Conduct on Mortgage Arrears, 2013 – Statutory Code

For those mortgages that are in arrears, or at imminent risk of becoming in arrears (known as ‘pre-arrears’), the Central Bank has published a Code of Conduct on Mortgage Arrears. This Code replaces the 2009, 2010 and 2011 Codes and, some would argue, contains reduced borrower protections, particularly compared to its 2011 predecessor.

There are no provisions in this Code dealing with the transfer of mortgages, however it is included here because it is referenced as a key piece of consumer protection for borrowers in arrears with which, since 2015/2018, credit servicing firms and loan owners registered as credit servicing firms with the Central Bank much comply.

However, a fundamental flaw with this Code demonstrates how a borrower may have two very different experiences with two loan owners (for this purpose, the existing loan owner and the new loan owner), notwithstanding that both are subject to the Code.

Provision 39 of the Mortgage Arrears Resolution Process provides (emphasis added):

In order to determine which options for alternative repayment arrangements are viable for each particular case, a lender must explore all of the options for alternative repayment arrangements offered by that lender.

It then goes on to list a suite of options that the lender may include. On this basis, if the existing loan owner offers the full suite of options and the new loan owner does not (which is particularly the case with non-bank entities), the borrower is disadvantaged by the transfer notwithstanding the application of the Code by both loan owners.

The lack of consistency in applying the Code has recently prompted the Central Bank to issue a letter to all regulated entities covered by the Code, dated 22 March 2019, reminding them of their obligations and requesting that certain information obligations be fulfilled. This Code is 6 years old this Summer and it is still not being fully implemented by those who have been working with it since its inception. What faith should we have that new entrants would be any more rigid in their appraoch?

Code of Practice on the Transfer of Mortgages, 1991 – the Voluntary Code

Although not a statutory code like the previous two, there exists a comprehensive Code of Practice on the Transfer of Mortgages published by the Central Bank in 1991. This Code effectively provided the blueprint for the Bill currently in discussion, setting out in full the requirements of sections 5 and 6 of the Bill. The Central Bank have recently stated this Code is no longer necessary, however its provisions have not been replicated in any subsequent statutory Code at a time when mortgage transfers are more prevalent than ever.

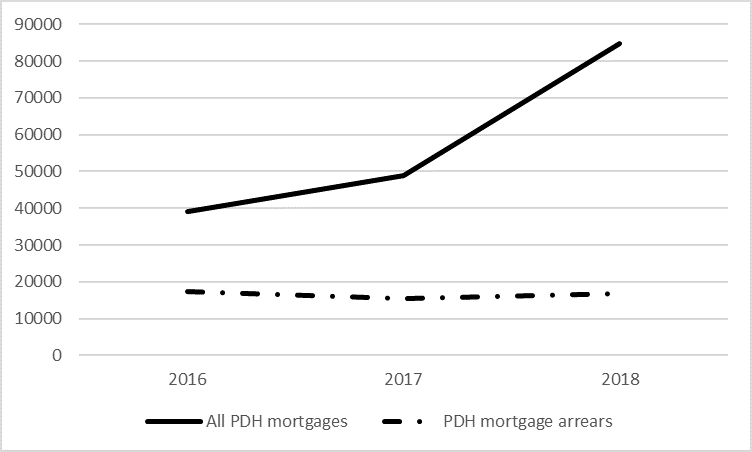

Data extracted from the Central Bank’s quarterly statistical report on mortgage arrears show that while the number of PDH mortgages held by non-bank entities has more than doubled since 2016 (an increase of 116%), the number in arrears has actually decreased slightly (Chart 1).

Chart 1: PDH Mortgages held and Mortgage Arrears, Non-Bank Entities, 2016 to 2018

Source: Central Bank of Ireland, Residential Mortgage Arrears and Repossession Statistics, March 2019.

Given the exponential increase in transfers to non-bank entities in recent years, it is vital that borrowers are given all available information to allow them to provide fully informed consent to the transfer of their mortgage. Social Justice Ireland supports the progression of the No Consent, No Sale Bill into law, amended to include information on restructuring options and reassurances that those available from the existing loan owner will continue to be available from the proposed loan owner.