Post-COVID-19: Basic Income, How it’s Paid for and How to Get There

What is a Universal Basic Income?

Briefly put, Universal Basic Income (UBI) is a universal non-conditional payment from government, paid regardless of income or wealth, at the same level to everyone in a specified age group. It is granted to every person on an individual basis, without means test or work requirement. Under most proposals it is tax-free, with all other personal income being taxed.

It could replace almost all weekly social welfare payments, as well as all tax credits and tax reliefs.

People can top up their income from other sources and, unlike under more traditional means-tested welfare systems, payment of UBI is not affected by changes in employment status. UBI differs fundamentally from the traditional welfare state model in that it is paid unconditionally, giving people the freedom to engage in productive activity without having to meet certain criteria as outlined by the welfare provider.

For more detail on exactly what Universal Basic Income is, see our most recent article here.

Eligibility and Structure

Social Justice Ireland has costed many versions of a Universal Basic Income over the past 25 years. For example, in our 2016 conference paper entitled Costing a Basic Income for Ireland, we proposed a partial Universal Basic Income starting at €150 per week, that was fair, efficient and sustainable. This paper was an exercise in showing how a UBI could be paid for in Ireland within current structures. It was not a paper advocating at what rate a UBI should be set, however the following are some of the basic eligibility conditions and details of that version of a partial UBI, which may be instructive in any debate on its introduction:

- Payment would be conditional on residency within Ireland. In line with current welfare requirements, non-citizens must have lived here for a number of years before becoming entitled to a UBI.

- The level of the payment would be age-dependent.

- Payment would be constant and does not change upon the taking up of employment or the acquiring of other income.

- All income, aside from the UBI payment, would be subject to tax at one single rate of 40 per cent. All other income tax rates, as well as Employee PRSI and Universal Social Charge, are abolished. The rationale for using a tax rate of 40 per cent was to show what could be achieved in the prevailing context in 2016. Raising the necessary funds on the basis of a more progressive taxation model would be preferable.

- The Employer PRSI rate would increase to 13 per cent.

- There would be no tax credits or tax reliefs.

- The UBI would replace almost all core welfare payments, payments in respect of disability, illness and other additional needs would be retained.

How it’s paid for

There are many ways a UBI could be funded sustainably. The most straightforward way of funding a UBI is through reform of the personal income tax and social welfare systems. Our research has shown that several types of basic income payments are possible simply through re-structuring the income tax system and abolishing or reconfiguring certain welfare payments to re-distribute money already within the system. There are several other approaches, however, that have been proposed. Here is a very short outline of three of these: capital taxation, taxing natural resources and consumption taxes.

Capital taxation

This is basically an approach that would tax capital more. This would reduce the gap between tax on labour income and capital income. This could be done by (1) increasing taxation on capital directly through a steeply progressive personal wealth tax or (2) by taxing capital income at a higher rate than at present. In practice, this is a tax on the stock of wealth or, alternatively, on the flow of income into wealth. A third option is to increase corporate taxation through, for example, a minimum effective corporate tax rate that in practice would only impact the large corporations who pay very low effective tax rates. A fourth option is through an inheritance tax.

Any or all of these options would have the effect of reducing the contribution that income tax would have to contribute and, consequently, reduce the required income tax rate.

Taxing natural resources

The first type of such a tax would focus on renewable natural resources on which there would be a tax or fee which would fund a UBI. The most obvious version of this approach would see an increase in land taxation. But it could also apply to other scarce permanent natural resources such as the broadcast spectrum that is now privately owned for the most part. Carbon taxes are another example of a tax on a permanent natural resource, the environment, which is being poisoned by our carbon dioxide emissions at present. This would have the double effect of funding a UBI while also protecting the environment.

Each of these could be seen as a fee for using a collectively owned asset rather than as a tax.

Consumption Taxes

This approach focuses on taxation on income as it is spent rather than when it is earned. One way of doing this is via the VAT system with which we are very familiar in Ireland.

In discussions about introducing an EU-wide (or Eurozone) Basic Income, proposals to have VAT as the main source of funding have been discussed for a quarter of a century. There is a major advantage to using a system such as VAT to provide a major component of the funding as, acknowleding the regressive nature of VAT on current income distribution, it would be more progressive to tax the expenditure than the current system which allows high earners to gain from deductions, tax breaks, loopholes, the separate taxation of capital income, various approaches aimed at maximizing tax avoidance as well as sheer tax evasion. VAT would capture a proportion of all expenditure.

Social Justice Ireland’s proposal

Social Justice Ireland’s proposed system of UBI involved the abolition of all core social welfare payments, with the retention of those supplementary welfare payments needed to ensure that the least well-off in society do not lose out unduly due to the introduction of the proposed system.

The proposed funding model also involved creating savings and efficiencies from certain parts of the welfare system (and from other government departments); removing certain payment types that are no longer required under the system; and the institution of a single tax rate on all income earned apart from the UBI payment.

Employer PRSI

In terms of Employer PRSI, Ireland lags far behind its developed western counterparts, with a rate (of 10.95 per cent) that is almost half the EU average (of 21.31 per cent)[1].

There is, therefore, plenty of scope for increasing the contribution made by employers to the system. Increasing the Employer PRSI rate from the current rate of 10.95% to 13% (just below that of the United Kingdom at 13.8 per cent) is a sensible and justified way to assist in funding a system of UBI.

Distributional Effect

Our UBI proposal would have a broadly positive effect, especially among lower income groups. Low-income earners would have very low effective tax rates when the un-taxed basic income payment is taken into account, and those on very low earnings would receive a top up to their gross wages.

Other Benefits of the Proposal

The proposed system of UBI would have many benefits compared to the current welfare system in Ireland, namely:

- The UBI system proposed would be far more easily administered, given the reduced number of payment types and the universality of payments. There would be a much-reduced need for means-testing and other time-consuming tasks, reducing the cost of administering the welfare system;

- UBI would eliminate the poverty traps inherent in traditional means-tested welfare systems. Employment is always worth pursuing, as the UBI will be received in addition to money earned through employment, rather than withdrawn, like most welfare payments under the current system. It is also untaxed;

- Welfare fraud would be more-or-less eliminated, as payment of UBI is not contingent on employment status or means;

- UBI respects and rewards all forms of work, not just paid employment. Caring work, home duties, and child-rearing – all socially and economically imperative work – would receive additional recognition under this system;

- UBI would assist in alleviating poverty, and with payments being universal, there would be no stigmatisation for recipients;

- UBI would be good for the environment, as it facilitates a society and an economy that does not have full paid employment as an overarching goal. Full employment relies on ever-expanding GDP growth, which conflicts with our concerns for the environment. UBI would reduce the extent to which the ability to live life with dignity is tied to labour market participation by a member of the household.

- In relation to the poverty traps which exist under the current Irish welfare system, the benefit of UBI was well summed up by Philippe Van Parijs when he said “it provides [poor people] with a floor on which they can stand, because it can be combined with earnings, rather than a net in which they can easily get stuck”[2].

So how do we get there?

Irrespective of how it is financed, there are a number of pathways that might be followed to introduce UBI in Ireland, and the main difference between them is timing. Some advocates propose an approach that would see the immediate implementation of a full basic income system once the required elements are in place; others propose an approach that would take place over a particular time period; and that time period can vary from three years[3] to twenty years[4] to even fifty years[5].

What follows is a brief overview of five different pathways to implement a UBI[6]:

- All-at-once approach

- By groups approach

- One step at a time approach

- Partial basic income approach

- Gradual approach

- All-at-once approach

The All-at-once approach

This involves the complete removal of the current system and the implementation of a full UBI at the same time. It would see the complete elimination of the current income tax and social welfare system, to be replaced by a basic income system. On the last day of the tax year, taxes and benefits would be collected and paid through the existing system. Then during the first week of the new tax year, taxes would be collected through the new system and UBI payments would be made.

The advantages of this approach are that it quickly eliminates the present tax and social welfare system and it quickly realises the benefits of basic income. It would prevent confusion arising from parts of the social welfare system being universal and parts still being means tested. The disadvantage is that the change required might be too drastic for some who would need to become gradually accustomed to receiving UBI payments. The ‘all-at-once’ option would require significant planning and system testing to ensure the transition to a basic income system does not cause disruption and does not have unintended consequences. A clear public education and information strategy over the months leading up to the change to a full basic income system would be necessary.

The ‘by groups’ approach[7]

This would involve the introduction of UBI payments to certain groups in society, one after the other. There are several ways of doing this. A ‘by groups’ basic income system could be progressed over a four year period by introducing a basic income for different groups in each of the four years. Clark and Healy[8] suggested that in year one, a partial basic income for adults aged 21- 64 be introduced. In year two, most of the children’s basic income would be introduced. In year three, a full basic income payment for older people would be introduced. In year four, the outstanding parts of the children’s and adult’s payments would be introduced. In order to implement a basic income system of this design in Ireland today the working age and older person’s basic income payment would have to be adjusted according to the new retirement ages and a fifth element would be required for young people aged 18 to 21.

The advantage of the ‘by group’ approach is that the level of change is not as dramatic as in the ‘all-at-once’ approach. The disadvantages of this approach are that there are winners and losers, as some groups go first and other groups have to wait a number of years. This could cause resentment between lifecycle groups as some go without a basic income but face increased tax rates for a number of years.

‘One step at a time’ approach

This approach is designed to move towards a full basic income system in increments. has the advantage of allowing space to test new approaches without causing too much disruption for household budgets or tax or benefit administration systems. The disadvantage is that the underlying issue of a benefits system not fit for purpose for today’s society is not resolved[9]. The most prominent proponent of this approach is Malcom Torry, whose proposal is concerned with children and young people and based on the UK system. He proposes that child benefit is turned into the child’s citizen’s income and that a young adult’s citizen’s income for young people aged 16-18 is established. The payment for young adults is then retained through adulthood. At the same time a citizen’s income for older people is introduced by turning the UK Single Tier Pension into a universal citizen’s pension. Torry estimates that this ‘one step at a time’ approach could deliver a full citizen’s income system in the UK in fifty years depending on the method adopted[10]. The main advantage of this approach is the gradual nature of the change. However, the disadvantage of this approach is that not everyone benefits from it.

Fitzpatrick[11] also proposed a ‘one step at a time’ method which would see a full UBI system being implemented over a twenty year period through the following five stages of implementation:

- revised social insurance

- social insurance plus transitional basic income

- participation income

- partial basic income, and,

- full UBI.

The argument is that the introduction of a full UBI ‘all-at-once’ would most likely be unacceptable in political discourse. A long-term approach would allow time for a basic income to garner political and social support and for voters to be persuaded of the value of basic income.

Partial basic income

A variation on the ‘one step at a time’ approach is the partial basic income pathway. This option involves giving a (usually modest) partial basic income to some or all citizens over a period of time which would gradually expand and increase over time until a full basic income system is developed. Proponents of this approach[12] argue that this is the most appropriate method to transition to UBI in the long term as the ‘all-at-once’ approach would be too disruptive and seen as politically unacceptable. The disadvantage of this method is that the welfare system is a mix of conditional and unconditional regimes for an extended period of time, with the challenge of how a partial basic income would interact with conditional welfare benefits and payments.

Another approach[13] proposes giving all citizens an unconditional tax credit as a partial basic income which could be built up gradually as rewards from work fall. A 2016 study considering possible UBI simulations concluded that a modified partial basic income, paid at a lower rate and retaining existing means-tested benefits, would be viable, although it would keep some of the complexities of the existing benefits system. The authors proposed that such a partial basic income could be introduced either by demographic group or by introducing modest, partial basic income payments which would be increased over time[14].

Gradual approach

And finally to the gradual approach to implementing a UBI which involves dismantling the current system while simultaneously building up the UBI system[15]. This approach would establish the UBI system separately from the current tax and welfare systems. It would see the gradual phasing in of the UBI system while the current tax and welfare systems are phased out. This would be done over whatever specific time period is chosen. The advantage of the gradual approach is that the challenge of reforming the current complex tax and welfare systems in order to move to a basic income system is overcome. The basic income system is established separately from the current tax and social welfare system. The gradual approach is equitable in that it distributes the costs and gains of the basic income system equally. It also avoids the disruption of the ‘all-at-once’ approach and the possible resentment between lifecycle groups of the ‘by group’ approach.

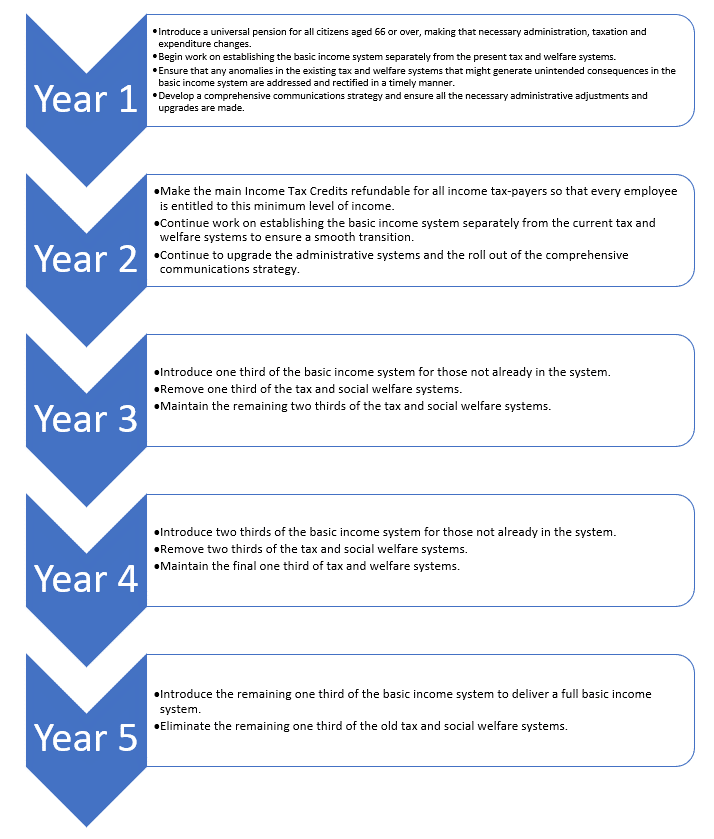

The Social Justice Ireland approach

Social Justice Ireland has advocated that a UBI system be implemented over a five-year period, that is, one Dáil term. We believe that a gradual approach over five years would be most appropriate in the Irish context given the complexity of the Irish tax system and the social welfare system and the reforms required to implement a basic income system. A five-year timeframe would also allow sufficient time to ensure that the basic income system is developed appropriately and that any anomalies within the current tax and social welfare systems and their interaction are addressed.

In order to deliver a structure that will support a basic income system in Ireland, two key reforms are required; one reform in the tax system and one reform in the social welfare system. By implementing these reforms the current tax and social welfare systems in Ireland would contain the necessary elements to provide a structure for a basic income system.

The two proposed reforms required to adjust the current tax and social welfare systems to support a basic income structure are:

- Make the State Contributory Pension a universal payment for all adults aged 66 years and above.

- Make the main income tax credits refundable.

These reforms could be implemented consecutively, and once implemented Ireland’s tax and social welfare system would be structured in a way that would support the gradual introduction of a basic income system.

Phasing In

In practice, if the State Contributory Pension was turned into a universal pension and if tax credits were made refundable then Ireland would have a structure that would support the implementation of a UBI system. The tax and social welfare systems would contain a universal entitlement for all stages of the lifecycle and every person in society. Older people would be entitled to the universal pension, children would be entitled to Child Benefit, and adults of working age would be entitled to a refundable tax credit or a social welfare payment. The level of these payments, of course, would vary. However, developing a structure that would support a universal entitlement for all stages of the life cycle through the tax and social welfare systems would allow for the transition to a basic income system.

A basic income system in Ireland could be introduced over five years (i.e. a Government term of office) if it were implemented as follows:

The value of a gradual five-year approach as proposed is that the necessary changes to the tax and social welfare systems are made so that they contain the essential elements for a UBI system. This would deliver a smooth transition. In year one and year two, people aged 66 and over and adults in employment gain the benefits of these reforms, and in years three to five everyone gets the initial benefits of the basic income payments in a gradual manner.

Conclusion

Ireland’s society is structured in such a way that the only way most people can live life with dignity is by having paid employment, or by living in a household where someone is in paid employment. Yet we have seen time and again how quickly that paid employment can disappear, most starkly with the current Covid-19 crisis. If paid employment cannot provide the basic floor for all citizens to live a life with dignity, then we must find an alternative. That alternative is the introduction of a UBI system in Ireland.

The standard objection to UBI is that it is unaffordable. But this depends largely on what parameters are set: the level of the payment; which benefits it replaces and which (if any) remain; what the eligibility conditions are, and so on. In our 2016 paper, Social Justice Ireland provided a structure, and a pathway, that was affordable within the existing system, sustainable and possible over a five-year period. We need now to look at how this might be implemented as part of a new Social Contract, in partnership with all stakeholders.

[1] https://home.kpmg/xx/en/home/services/tax/tax-tools-and-resources/tax-ra...

[2] https://www.socialeurope.eu/44878

[3] Clark, C. M.A. and Healy, J (1997): Pathways to a Basic Income. Dublin: CORI

[4] Fitzpatrick, T (1999): Freedom and Security: An Introduction to the Basic Income Debate. Basingstoke: Palgrave Macmillan.

[5] Torry, M (2015): Two feasible ways to implement a revenue neutral Citizen’s Income Scheme. Euromod Working Paper Series EM 6/15

[6] For more detail on each of these pathways, see our 2016 paper ‘Pathways to a Basic Income System’.

[7] Also known as the demographic approach

[8] Clark, C.M.A. and Healy, J (1997): Pathways to a Basic Income. Dublin: CORI

[9] Torry, M (2015): Two feasible ways to implement a revenue neutral Citizen’s Income Scheme. Euromod Working Paper Series EM 6/15.

[10] The introduction of an unconditional pre-retirement payment for everyone over 55 would shorten the timeframe by thirteen years.

[11] Fitzpatrick, T (1999): Freedom and Security: An Introduction to the Basic Income Debate. Basingstoke: Palgrave Macmillan

[12] Groot, LFM (1999): Basic Income and Unemployment. Utrecht: Netherlands Schools of Social and Economic Policy Research.

[13] Skidelsky, R (2015): Minimum Wage or Living Income? Project Syndicate.

[14] Reed, H and Lansley, S (2016): Universal Basic Income: An idea whose time has come? London: Compass.

[15] Clark, C.M.A. and Healy, J (1997): Pathways to a Basic Income. Dublin: CORI