Refundable Tax Credits key to helping the working poor

It has become cliché at this point to say that the Covid-19 pandemic has caused significant re-examination of how we have structured our society and economy. More than ever, it seems that policymakers are expressing an appetite for new ideas and new policies. Social Justice Ireland believes that by omitting Refundable Tax Credits from the proposed Programme for Government, a huge opportunity has been missed to tackle in-work poverty and make the Irish income tax system fairer.

As we has been pointing out for several years, Ireland has a persistent problem with in-work poverty. Each year, when the Central Statistics Office publishes Ireland's updated poverty numbers, there is little change in the number of people in employment who are at risk of poverty. In 2018 - the latest years for which statistics are available - there were approximately 109,000 people with jobs who were living in poverty. Many people assume that a job is an automatic poverty reliever but this is clearly not the case. The job must also be a well-paid job, and emerging trends of precarious working practices must surely contribute to a situation where more than 5 per cent of those in employment are still experiencing poverty.

Specific interventions are required to tackle the problem of the ‘working-poor’. Social Justice Ireland warmly welcomed the inclusion in the Fianna Fáil-Fine Gael draft document for government negotiations of a commitment to create a Living Wage within the term of the next government. Refundable Tax Credits can also play a key role. Until Government makes tax credits refundable, it will not have an efficient mechanism by which it can address the issue of the working poor.

Making tax credits refundable would make Ireland’s tax system fairer, address part of the working poor problem, and improve the living standards of a substantial number of people in Ireland.

What are Refundable Tax Credits?

Whether you are working part-time for a few hours each week or are in a very high paid job, everyone who is in employment in Ireland has tax credits. Once an individual's tax liability has been calculated, these credits are applied in order to bring down their tax bill. However, if a low income worker does not earn enough to use up their full allocation of tax credits then they will not benefit from any income tax reductions introduced by government in the annual budget via increases to the PAYE or Personal tax credits.

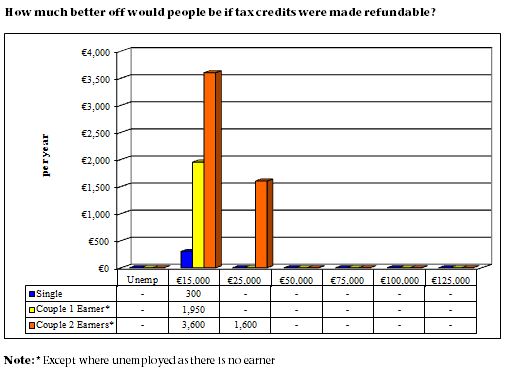

Making tax credits refundable would be a simple solution to this problem. It would mean that the part of the tax credit that an employee did not benefit from would be “refunded” (essentially paid, at the end of the tax year) to him/her by the Revenue Commissioners. The major advantage of making tax credits refundable lies in addressing the disincentives currently associated with low-paid employment and the main beneficiaries of refundable tax credits would be low-paid employees (both full-time and part-time). The chart below displays the impacts of the introduction of this policy across various gross income levels. It clearly shows that all of the benefits from introducing this policy would go directly to those on the lowest incomes.

Most people with regular incomes and jobs would not receive any cash refund because their incomes are too high. They would simply continue to benefit in the same way as before from any increase to tax credits, via a reduction in their tax bill. Therefore, as the above chart shows, no change is proposed for these people. For other people on low or irregular incomes, the refundable tax credit could be paid via a refund by the Revenue Commissioners at the end of the tax year. There may even be scope for more real-time delivery of the benefit, given the new real-time reporting systems in place at Revenue in the last few years.

Following the introduction of refundable tax credits, all subsequent increases in the level of the tax credit would be of equal value to all employees.

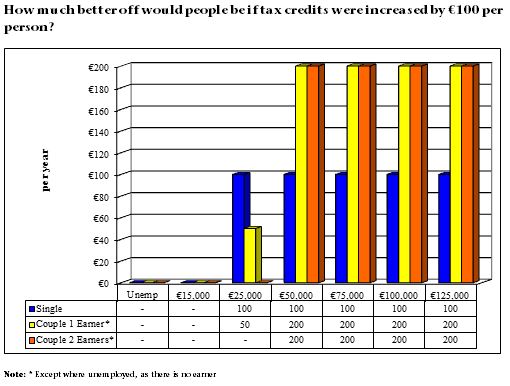

To illustrate the benefits of this approach, the charts below compare the effects of a €100 increase in the personal tax credit before and after the introduction of refundable tax credits. The first shows the effect as the system is currently structured – an increase of €100 in credits that are not refundable. It shows that the gains are allocated equally to all categories of earners above €50,000. However, there is no benefit for those workers whose earnings are not in the tax net.

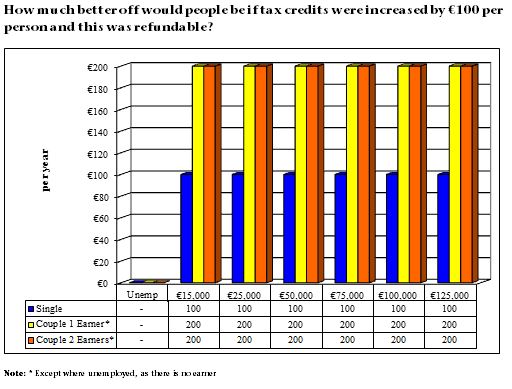

The second chart shows how the benefits of a €100 a year increase in personal tax credits would be distributed under a system of refundable tax credits. This simulation demonstrates the equity attached to using the tax-credit instrument to distribute budgetary taxation changes. The benefit to all categories of income earners (single/couple, one-earner/couple, dual-earners) is the same. Consequently, in relative terms, those earners at the bottom of the distribution do best.

Among the merits of adopting this approach are:

- that every beneficiary of tax credits would receive the full value of the tax credit;

- that the system would improve the net income of the workers whose incomes are lowest, at a modest cost;

- that there would be no additional administrative burden placed on employers.

In 2010 Social Justice Ireland published a detailed study on the subject of refundable tax credits. Entitled Building a Fairer Tax System: The Working Poor and the Cost of Refundable Tax Credits, the study identified that the proposed system would at that time benefit 113,000 low-income individuals in an efficient and cost-effective manner. When children and other adults in the household are taken into account the total number of beneficiaries would be 240,000. The cost of making this change would be €140m. The Social Justice Ireland proposal to make tax credits refundable would make Ireland’s tax system fairer, address part of the working poor problem, and improve the living standards of a substantial number of people in Ireland. The following is a summary of that proposal:

Making tax credits refundable: the benefits

- Would address the problem identified already in a straightforward and cost-effective manner.

- No administrative cost to the employer.

- Would incentivise employment over welfare as it would widen the gap between pay and welfare rates.

- Would be more appropriate for a 21st century system of tax and welfare.

Details of Social Justice Ireland proposal

- Unused portion of the Personal and PAYE tax credit (and only these) would be refunded.

- Eligibility criteria is applied to the relevant tax year.

- Individuals must have unused personal and/or PAYE tax credits (by definition).

- Individuals must have been in paid employment.

- Individuals must be at least 23 years of age.

- Individuals must have earned a minimum annual income from employment of €4,000.

- Individuals must have accrued a minimum of 40 PRSI weeks.

- Individuals must not have earned an annual total income greater than €16,500.

- Married couples must not have earned a combined annual total income greater than €33,000.

- Payments would be made at the end of the tax year.

Cost of implementing the proposal

The total cost of refunding unused tax credits to individuals satisfying all of the criteria mentioned in this proposal was estimated at €140m.

Major findings

At the time of the study, it was estimated that:

- Almost 113,300 low income individuals would receive a refund and would see their disposable income increase as a result of the proposal.

- The majority of the refunds would be worth under €2,400 per annum, or €46 per week, with the most common value being individuals receiving a refund of between €800 to €1,000 per annum, or €15 to €19 per week.

- Considering that the individuals receiving these payments have incomes of less than €16,500 (or €317 per week), such payments are significant to them.

- Almost 40 per cent of refunds would flow to people in low-income working poor households who live below the poverty line.

- A total of 91,056 men, women and children below the poverty threshold would benefit either directly through a payment to themselves or indirectly through a payment to their household from a refundable tax credit.

- Of the 91,056 individuals living below the poverty line that benefit from refunds, most, over 71 per cent receive refunds of more than €10 per week with 32 per cent receiving in excess of €20 per week.

- A total of 148,863 men, women and children above the poverty line would benefit from refundable tax credits either directly through a payment to themselves or indirectly (through a payment to their household. Most of these beneficiaries have income less than €120 per week above the poverty line.

- Some 240,000 individuals overall, all of whom are living in low-income households, would experience an increase in income as a result of the introduction of refundable tax credits.

Once adopted, a system of refundable tax credits as proposed in this study would result in all future changes in tax credits being equally experienced by all employees in Irish society. Such a reform would mark a significant step in the direction of building a fairer taxation system and represent a fairer way for Irish society to allocate its resources.