Increase in Financial Distress likely post-COVID-19

Increase in Financial Distress likely post-COVID-19

Over one million people were in receipt of COVID-19-related income supports as of May this year. 584,641 were in receipt of the Pandemic Unemployment Payment (PUP) and 473,500 people had availed of the Temporary Wage Subsidy Scheme (TWSS)[1]. These numbers have been decreasing as the economy slowly starts to open again, those who needed to avail of loan repayment breaks and rent freezes will face likely financial distress.

In 2018, almost four in ten people (37.3 per cent of the population) reported being unable to face an unexpected financial expense[2].

Those whose employment was affected by COVID-19-related closures accounted for more than one in five workers (21.2 per cent), with earnings in many of these sectors being lower than the average national wage[3]. Households dependent on these incomes are less likely to have capacity to save and are therefore more susceptible to financial shocks. The Household Finance and Consumption Survey indicates that households in the lowest quintile of the income distribution were less likely to have savings than those on higher incomes, with the median value of these savings being €2,000[4].

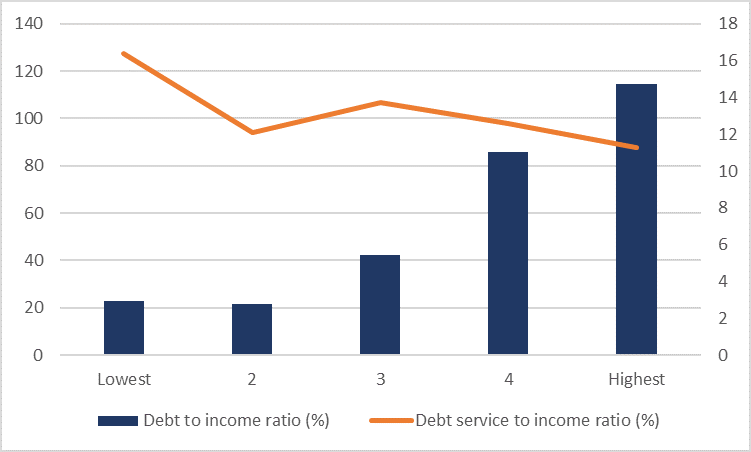

While the debt-to-income ratio[5] of households in the bottom quintile are significantly lower than those on the highest incomes, the debt service-to-income ratio[6] is over five percentage points higher (Chart 1).

Chart 1: Debt-to-Income Ratio and Debt Service-to-Income Ratio by Income Quintile

Source: CSO, Household Finance and Consumption Survey, Statbank Table HFC31

This means that debt repayments account for a higher proportion of the household income of lower income households than that of higher income households. These households are less likely to have sufficient savings to make debt repayments if they are out of work, and while the PUP covered between 70 and 100 per cent of net wages in the retail, recreation and hospitality sectors, it accounted for just 56 per cent of net earnings in construction and 52 per cent in manufacturing[7].

Mortgage Debt

Over 17 per cent of all primary dwelling house mortgages were restructured and/or in arrears as of 31 December 2019. Mortgage accounts that have been restructured are deemed to be more vulnerable to financial shocks and have higher mortgage repayment to income ratios than other mortgages[8]. While mortgage holders are less likely to work in sectors impacted by COVID-19, the income shock will have a significant impact on mortgage borrowers with higher mortgage to income ratios. Models developed by the Central Bank indicate that borrowers with high mortgage payment burdens in excess of 30 per cent of gross income could increase from 10 to 15 per cent. Should the COVID-19 income supports be reduced to the basic Jobseeker’s rate of €203, this proportion would increase further to an estimated 23 per cent.

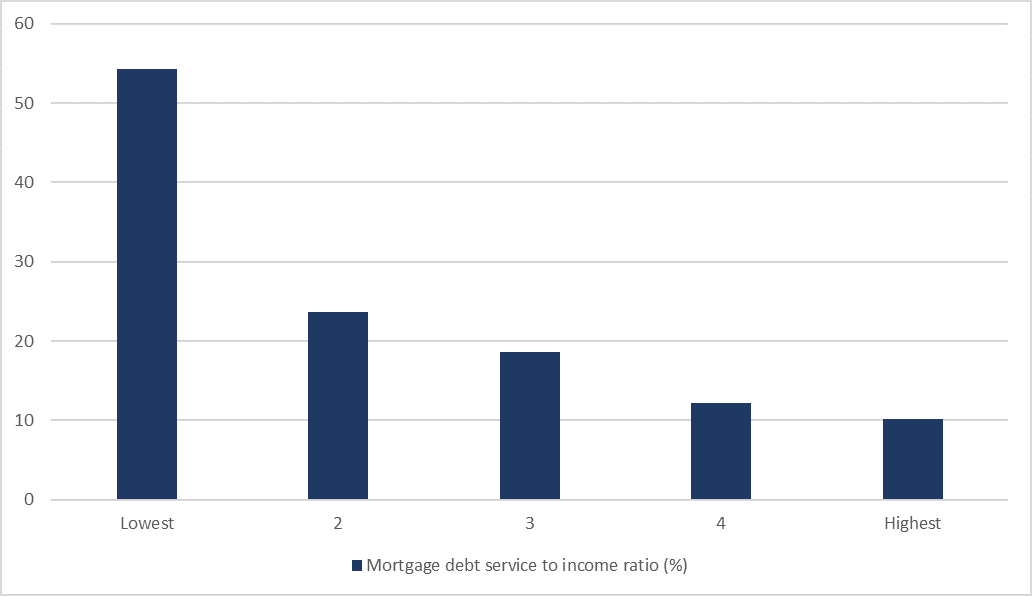

For mortgage borrowers in the lowest income quintile, the mortgage debt service-to-income[9] ratio is already 54.3 per cent (Chart 2).

Chart 2: Mortgage Debt Service-to-Income Ratio by Income Quintile

Source: CSO, Household Finance and Consumption Survey, Statbank Table HFC31

Rent Payments

The prohibitions on evictions from rental properties and private rent increases, introduced in March this year, were extended to the 20th July. This, on the face of it, is good news. However while landlords cannot evict tenants or increase their rent during this time, the rent is still due. Tenants can apply for rent supplement, however where this is delayed or not approved, those tenants are still expected to pay their rent and rent review notices notifying tenants of an increase can still be served (although the increase can only take effect after the emergency period has ended).

Over 14 per cent of tenants paying market rent were spending more than 40 per cent of their disposable household income on housing costs in 2018[10]. Add to that a decrease in income of up to 48 per cent and the accumulation of rent arrears and this becomes completely unsustainable.

Tenants, particularly those in low paid or precarious employment, were in crisis before COVID-19. A rent debt crisis is the culmination of years of poor policy and inadequate protection.

Other debts

Mortgage and rent are likely to be the largest payments faced by most households. However, the percentage of households with non-mortgage loans is 30.4 per cent, with 12.7 per cent of all households having credit card debt[11]. Almost 9 per cent of the population reported being in arrears on utilities and 2 per cent reported arrears on hire purchase or other loans[12].

The data available from the Central Bank and the EU-SILC survey relates to “formal” sources of credit. For many low-income households, restrictions on borrowing from mainstream lenders and an inability to provide for contingency savings means finding alternative sources of credit. A report from the Social Finance Foundation found that in 2018 there were 330,000 people accessing credit from moneylending firms[13]. The majority of were female, aged between 35 and 54 and drawn from lower socio-economic backgrounds. A large proportion have loans from ‘home credit companies’ which charge APRs of up to 287 per cent. These alternative sources of credit are often prioritised, irrespective of interest rate or associated risks, as providing easier access to emergency funds and a personal connection with the creditor[14].

Need for Real Solutions

Social Justice Ireland has previously called for the establishment of a Personal Debt Taskforce to support households with problem debt, particularly low income households.

We were disappointed that measures to tackle problem non-mortgage debt were not included in the Programme for Government.

We do, however, welcome the inclusion of an assessment of the Code of Conduct on Mortgage Arrears as a first step in strengthening consumer protection and reversing the move to reduce these protections following its revision in 2013.

We also welcome the inclusion of reforms to the personal insolvency legislation, which is not fit for purpose and has only served to create yet another private industry being supplemented by the State. In this regard, the commitment to continue funding for the Abhaile mortgage arrears project without a comprehensive cost-benefit analysis is regrettable.

The Programme for Government also made reference to the creation of a system for the holding of rental deposits. The legislation for this system already exists. It was introduced in 2015 and awaits commencement[15]. Additional supports will be needed for tenants in arrears as a result of COVID-19 reductions in income to avoid mass evictions for non- or part-payment of rent arrears.

The provision of real solutions to problem personal debt must start with financial literacy. As a start, the Money Matters (Junior Certificate) and Money Counts (Leaving Certificate Applied) financial literacy courses provided by the Consumer and Competition Protection Commission (CCPC)[16] should be integrated into the main curriculum, with basic programmes developed for primary school students. The Money Skills for Life talk, also provided by the CCPC, could also form part of orientation for third level education programmes.

There is also a need for low-cost credit, as an alternative to moneylending, for low-income households. The It Makes Sense Loan, available through participating credit unions[17], was a step in the right direction and similar offerings through the post office network could be explored to make it more widely available.

New Progress Index

Social Justice Ireland previously welcomed the commitment in the Programme for Government to include wellbeing indicators in addition to economic indicators to measure Ireland’s progress. Creating a sustainable Ireland requires the adoption of new indicators to measure progress. To reflect this, the wellbeing indicators that the new Government has committed to developing must include new indicators measuring both wellbeing and sustainability in society, to be used alongside measures of national income like GDP, GNP and GNI. Financial resilience must be one such indicator given the impact of debt on mental and physical health[18].

[1]https://www.centralbank.ie/docs/default-source/publications/financial-stability-review/financial-stability-review-2019-i/financial-stability-review-2020-i.pdf?sfvrsn=4 and Chart Pack

[2] Eurostat Database [ilc_mdes05]

[3]https://data.oireachtas.ie/ie/oireachtas/parliamentaryBudgetOffice/2020/2020-03-30_employment-in-sectors-exposed-to-the-covid-19-pandemic_en.pdf

[4] CSO Statbank: HFC10: Household Financial Assets by Percentile of Household Income, Type of Financial Asset, Year and Statistic

[5] The ratio between total liabilities and total gross income for indebted households. It is expressed as the (weighted) median. Households with zero debt are excluded from the calculation.

[6] The ratio between total monthly debt payments and household gross monthly income for indebted households. Households with zero debt are excluded from the calculation.

[7]https://data.oireachtas.ie/ie/oireachtas/parliamentaryBudgetOffice/2020/2020-03-30_employment-in-sectors-exposed-to-the-covid-19-pandemic_en.pdf

[8]https://www.centralbank.ie/docs/default-source/publications/financial-stability-review/financial-stability-review-2019-i/financial-stability-review-2020-i.pdf?sfvrsn=4 and Chart Pack

[9] The ratio between the mortgage debt service repayments of a household to the income of that household, for households with mortgage debt. Households with zero income are excluded from the calculation.

[10] Eurostat, Statbank [ilc_lvh028]

[11]https://www.cso.ie/en/releasesandpublications/ep/p-hfcs/householdfinanceandconsumptionsurvey2018/debtandcredit/

[12]Eurostat Database [ilc_mdes07, ilc_mdes08]

[14] Collard, S. and Kempson, E. (2005): Affordable credit for low-income households, University of Bristol

[15] The Residential Tenancies (Amendment) Act, 2015

[16]https://www.ccpc.ie/business/about/financial-education/

[17]https://itmakessenseloan.ie/

[18] Mental Health Commission, 2011: The Human Cost, An overview of the evidence on economic adversity and mental health and recommendations for action. Mental Health Commission: Dublin